ESG Economist - How feasible are the Dutch plans for nuclear power?

Nuclear power is set to play an essential role in providing supply flexibility, even as renewables dominate the power mix. In the Netherlands, there is now only one nuclear power plant operating. The Borssele nuclear power plant was built in early seventies with a capacity around 0.51 GW that produces around 400 GWh per year, enough to power one million houses, representing almost 3% of the Dutch power mix in 2023. As the Netherlands switches to a CO2-free electricity mix, nuclear is one of the pillars for the energy future of the country. Within its National Energy Plan (NPE), two new nuclear power plants are expected to be built and start operating by 2035 and 2037 respectively, with possibility for Dutch nuclear installed capacity to reach 7 GW by 2050. Furthermore, within the current political environment, that leans more to the right, there are proposals for a bigger role for nuclear power by extending the number of new plants to four nuclear plants. This note zooms into nuclear power in general, the current status of nuclear power in the Netherlands, the pros and cons associated to its development, the different generations of nuclear reactors, and examines the feasibility of current proposals for a bigger role in the future Dutch power mix.

Nuclear power is set to play an essential role in providing supply flexibility as renewables dominate the power mix

There are many advantages to nuclear power such as the highest spatial-efficiency and potential capacity factor compared to renewable sources, while safety, justice and the environmental concerns remain among the prominent challenges

New generations of nuclear power with advanced technology, strengthened safety measures, and new features are promising, putting nuclear back on the energy map in many countries

Lack of appropriate skills, special financing, along with constrained potential sites for nuclear plants are among the challenges for the development of nuclear capacity in the Netherlands

Within these challenges, the feasibility of extending nuclear capacity to add four new plants is questionable

Pros and cons of nuclear power for the Netherlands

The future Dutch power mix is going to be heavily reliant on solar and offshore wind. However, the intermittency of these resources increase vulnerability to weather conditions and more flexible capacity is therefore required. Nuclear power could play an important role in providing a stable and reliable base supply. Moreover, space wise, nuclear power has the least requirements per unit of electricity generated. It is the most spatially-efficient among other “green” power sources, and thus, helps in limiting the space associated to the future renewable power system. Furthermore, nuclear power has the highest capacity factor (1) among other “green” power sources. Also, nuclear power offers a stable source of electricity with no dependence on imported fossil fuels, which would help to achieve strategic energy independence.

Nuclear power also has disadvantages. It takes a long time to build a nuclear power plant, while there is a need for careful integration. Furthermore, safety is traditionally the most prominent concern about nuclear power especially after nuclear disasters such as Chernobyl and Fukushima have fuelled public concerns about this power source. Furthermore, from safety, justice and the environmental perspectives, it is of utmost importance to achieve adequate permanent storage of radioactive waste. This waste in the Netherlands is currently temporarily stored at the internationally highly regarded COVRA facility (see more ).

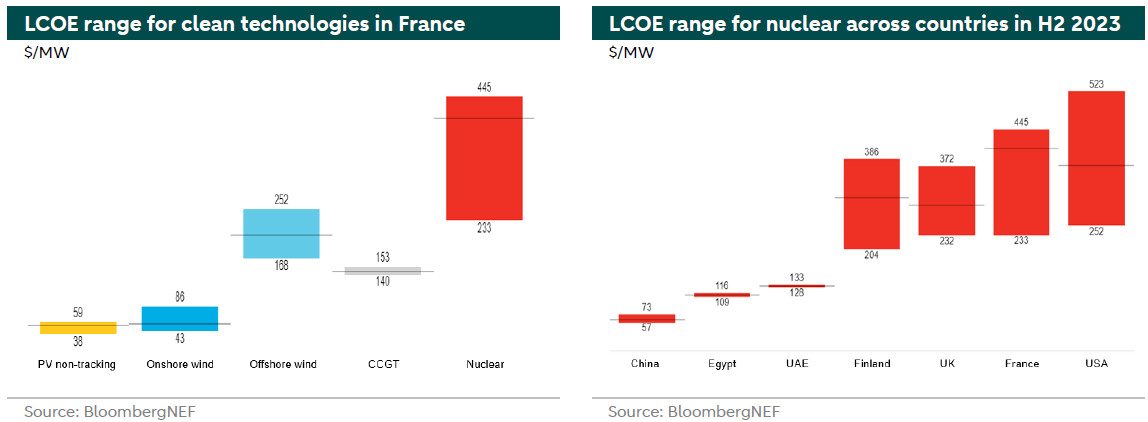

The figure above illustrates how the cost of nuclear power development, reflected by the Levelized Cost of Electricity (LCOE), stands in comparison with the cost of other renewable technologies (left hand chart) and across countries (right hand chart). The charts depict a higher cost and a wider range for nuclear than other technologies along with higher costs for development in more developed countries vis a vis developing/emerging economies. Illustrating the cost uncertainty associated to nuclear power development in Europe.

New generations of nuclear power, such as SMRs, with advanced technology, strengthened safety measures, and new features are promising, putting nuclear back on the energy map in many countries.

Different generations of nuclear reactors

Traditional nuclear power relies on fission reaction to boil water and generate steam. The fission splits uranium atoms into smaller atoms inside the nuclear reactor. The steam moves turbines that generate power. There are four generations of nuclear reactors. The first generation of nuclear reactors was developed during the fifties and the sixties. They mark the beginning of civil nuclear power and represent the prototype of nuclear reactors. Generation II reactors were designed to be economical and reliable with an average lifespan of 40 years. They started operating in the late sixties. Most of Generation II reactors are Light Water Reactors (LWRs), which is one type of Water Cooled Reactors (WCR) that use water as main coolant. Moreover, Generation II reactors feature traditional active safety measures that are activated passively (automatically) or by human intervention. However, Generation II designs require relatively large electrical grids and high safety standards and produce high quantities of radioactive waste that need careful and special treatment (see more ). Generation III reactors are an updated version of Gen II with state of the art design improvements that improved safety systems, fuel technology, thermal efficiency, modularized construction, standardization, and at least 60 years of operational lifetime. There are also Gen III+ reactors which come with further enhanced safety features.

Small Modular Reactors (SMR) are third generation reactors. Contrary to other generations, these reactors are small in size (could be 5 meters in diameters and 10 meters in height) and could be produced offsite and transported to facilities, which gives them huge advantages in terms of flexibility. They typically have less than 300 MW in capacity (see more ). SMRs are still at their early development stage with only one 35MW reactor currently operating on a floating power plant deployed by Russia in the Arctic in 2020.

SMRs could ultimately provide a safe and smart source of power if they can overcome challenges related to economics, safety and public opinion. More precisely, the development of SMRs is still not competitive with the cost of electricity produced by SMRs up to 10 times higher than the cost of electricity produced by fossil fuels. When comparing SMRs to large-scale batteries, that serve as at-the-ready backups for solar and wind power, SMRs look more attractive. From a safety perspective, some designs of SMRs use molten salt and metals to cool the reactor, as opposed to water in previous types. SMRs also integrate new kinds of fuel and backup emergency systems that decreases the likelihood of a meltdown. On the other hand, SMRs could be located nearer to city centres which worsen the consequences of any incident. Additionally, the lower power output allows SMRs to operate in connection to grid or in a standalone mode, which could help meting specific industrial or rural demand. Furthermore, plants that operate on SMRs require less frequent refuelling compared to their traditional counterparts. Some SMR designs feature the operation of the reactor for 30 years without refuelling.

Microreactors are a subset of SMRs that have a capacity of 10 MWe. Microreactors are appropriate for remote uses and backup power supply. SMR have a cost advantage where the unit cost of serially produced reactors could be lower by 30% than the costs of the first reactor, according to the IEA.

Other types of reactors could rely on other coolants such as helium coolant, also known as gas-cooled reactors. Almost all of such reactors exist in the UK and are planned to be shut down during this decade. China, however currently operates a High-temperature gas-cooled reactor (HTGC), which is a one type of gas-cooled reactors that produces very high core temperatures using uranium and graphite moderation. Such high temperatures allows for applications such as hydrogen production and process heat. A development of HTGC is the Very High Temperature Reactor (VHTR), which represents the fourth generation of future reactors.

Global and European nuclear power

There are approximately 442 reactors worldwide, which supply almost 10% of the power in the world. Almost 96% of existing nuclear power plants are second generation water-cooled reactors that have been built after the second world war. These reactors are aging with history of meltdowns and radioactive waste, which triggered public resistance to nuclear power. However, given the advantages of third generation SMRs, and the urgency to achieve climate targets and the green status for nuclear energy, there more support for SMRs in the EU.

In Europe, nuclear power is classified as a green energy source, and accordingly, European nuclear capacity is expected to reach 150 GW by 2050. To achieve this target, a new additional 50 GW of nuclear power should be added to the current 100 GW. This can be translated to 30-45 large reactors besides other Small Modular Reactors (SMRs) (see more ). In this direction, the European commission has been managing the formation of European Industrial alliance on SMRs to facilitate cooperation and knowledge exchange that accelerate the development, demonstration, and deployment of SMRs in Europe (see more ). Accordingly, many European countries have set up plans and roadmaps for their nuclear capacity. For example, in January the UK government launched its roadmap for nuclear energy with the aim to expand the current 5.8 GW capacity to 24 GW by 2050, through a combination of large and small reactors.

Current challenges to nuclear power in the Netherlands

There are multiple challenges to the development of nuclear power in the Netherlands. First, a lack of expertise generally and a skilled, knowledgeable work force specifically. Nuclear power is a very intricate process that requires specialised skills. Such skills are very particular and need time to develop. This will require attention to the required supply chains and the development of specialized, joint exchange, programs for technicians and engineers.

Also, given that offshore wind and nuclear power are going to represent big chunk of the future CO2-free energy mix in the Netherlands, and given the needed grid connection requirements, two large-scale forms of generation cannot simply be connected to the grid close to each other. Accordingly, a good network fit of nuclear energy in relation to the realization of offshore wind energy is important, putting more constraints on the development of nuclear facilities in the Netherlands.

To account for these challenges, the Dutch government acknowledges the added value of bilateral cooperation as different countries develop their nuclear capacity with different stages of development, exchanging expertise that would prevent repeating the same mistakes and associated costs. Moreover, the government acknowledges the gap in skills and the needed nuclear knowledge, and thus dedicated EUR 65 million to invest in nuclear skills and the build-up of the needed knowledge infrastructure (see more ).

How feasible are the Dutch plans for nuclear power?

The Netherlands is counting on nuclear power in the future energy mix to provide flexibility to the grid as solar and offshore wind will dominate the power mix in 2050. Currently, there is only one nuclear plant in operation, which is located in Borssele, in the southwest of the country. The operation of the current plant is to be extended. The government allocated EUR 10 million for this extension to be used between 2023-2025. The plan is to build two new nuclear power plants close to the current one in Borssele. However, the final decision on their location will only be made by the end of 2024. Initially, the government allocated EUR 5 billion euros to fund these plants out of the EUR 35 billion dedicated for the energy transition until 2030. The construction of the new plants is expected to start by 2028, and based on initial plans, the completion will be in around 2035. Each of these plans will have a capacity between 1000 and 1650 MWe and provide 9-13% power produced in the Netherlands.

The current political environment in the Netherlands is quite uncertain and a new coalition is in the making. Recent elections witnessed the rise of the right wing with programs envisioning an even a bigger role of nuclear power in the country. For example, the winning PVV party’s energy plan aims to build four new nuclear power plants instead of the current plan of two. The feasibility of such a plan is however questionable, especially after the publication of a new report by an expert team, that in April 2023, contested the future of nuclear power in the Netherlands and concluded that nuclear power would have a limited role in the Dutch energy mix and that the build of the nuclear plants would put big pressure on the grid, especially if these plants were built in the proposed location at the Borssele site. The current exiting government promised to investigate this further, but emphasized the need of nuclear energy in the country (see more ). Accordingly, choosing appropriate locations that takes into account the safety, security, environmental and social impacts and grid connection is one of the main challenges for nuclear power in the Netherlands

One other major challenge for nuclear power in the Netherlands is financing. For nuclear projects, the participation of the government is essential to lift these projects off ground, this is mainly due to the risks associated with every phase of a nuclear plant’s lifespan. According to a recent report on Dutch nuclear power financing (see ), private investors will not bear risks that they cannot control, for example risks associated to the delays in construction which could cause cost overruns, or the risk of early closure and associated decommissioning costs, along with risks of potential delays in permitting, political risks. The report thus emphasize the role of the state to share and mitigate these risks. This would be through the use of different financing models such as Contracts for Difference (CfD), Power Purchase Agreements (PPAs), or even the direct state ownership, or a combination of such models. This challenge will become more prominent with the plan of extending the Dutch nuclear capacity by four power plants, especially given the associated costs and the required budget from the Dutch government.

(1) Capacity factor refers to the amount a power plant can produce compared to its maximum potential (yearly) output.