ECB to put exit decision on hold amid risks

The Governing Council meets this week for its March monetary policy meeting. At the February press conference, the ECB signalled an exit trajectory, which made it seem likely that net purchases under the APP would end this year, and a rate hike would follow not long after that.

That seems like a long time ago now. Russia’s invasion of Ukraine has triggered a number of economic shocks as well as a high level of uncertainty about how severe the situation will get. On balance, we think these shocks will make the ECB follow a more accomodative policy compared to the pre-conflict scenario. Although sky-rocketing energy prices will raise inflation (even further) as well as hitting demand over the next year or so, we judge that the medium term consequences for the outlook are disinflationary.

How will the ECB proceed against this background? We think the central bank will move back to basing itself more on a scenario approach. We expect the base case to show inflation around its target over the 2-3 horizon, as well as above target in the coming quarters. Meanwhile, measures of underlying inflation have also risen, albeit still linked to supply shocks/Covid and with wages still subdued. Taking all this together, the ECB’s macro base case would still be consistent with an exit strategy. However, the central bank will also likely present an alternative – more negative scenario – with a bigger hit to the economy, which would show an under-shoot of its inflation goal over the medium term.

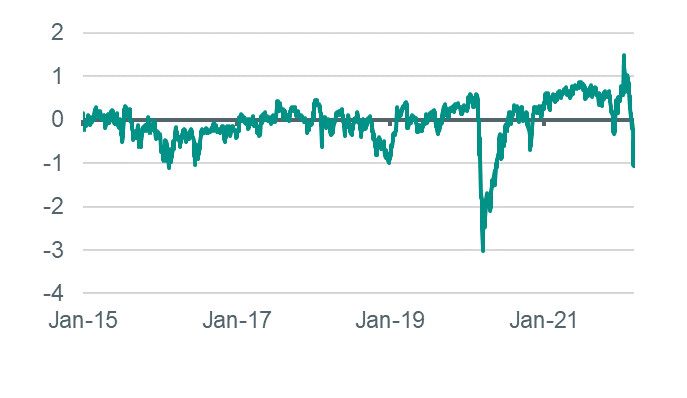

Eurozone financial conditions

Index (positive value indicates accomodative conditions)

Source: Bloomberg

Given this alternative scenario and the level of uncertainty, we expect the ECB to leave its trajectory for net asset purchases under the APP (EUR 40 bn in Q2, EUR 30bn in Q3 and EUR 20bn beyond that if necessary) unchanged. The significant tightening of financial conditions over recent weeks, also makes the case to put off the exit decision. The ECB would signal extreme flexibility and optionality going forward. If the uncertainty fades, so that the GC has more confidence in its base case and the risks of the alternative ease, then it could go ahead and announce a winding down of net purchases. However, if the risks of the negative scenario rise further, then a step up of net purchases would also be an option. (Nick Kounis & Aline Schuiling)