Does yield curve inversion mean a recession is coming?

The yield curve briefly inverted on Tuesday, which has in the past suggested a recession was looming. We view the inversion as little cause for alarm by itself, given that term premium is currently depressing long term bond yields. Instead, the near-term spread looks to be a better indicator of recessions, and this currently suggests a low recession probability. However, it doesn't rule out a recession either.

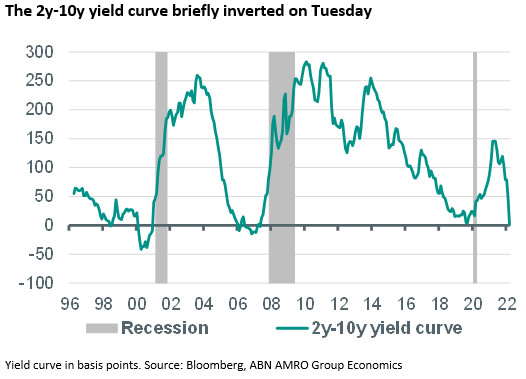

Curve inversion is not (necessarily) something to worry about

The spread between the US 2y and 10y Treasury yield briefly ‘inverted’ (i.e. the 2y yield was higher than the 10y yield) late on Tuesday, sparking fears among some market participants that the US economy may be heading for a recession. This is because, , the inversion of the yield curve has been a strong leading indicator of recessions, the idea being that it is a sign the market is pricing in a rate cut cycle (which a recession would trigger). Indeed, when an inversion is sustained over a sufficiently long period – at least one month (which is not the case now) – it has predicted all recessions of the past 50 years. There is a problem with interpreting yield curve inversions recently, however, and that is term premium: the compensation investors demand for the risk involved in holding securities over a long period. Term premium has been depressing long-term yields for at least the past 5 years, for much of which it has been negative (i.e. investors have been paying for the privilege of holding Treasurys for a long time period rather compensated). The most plausible explanation for negative term premium is quantitative easing by central banks, which as a policy has had the explicit goal of lowering long term bond yields. This significantly muddies the signal from the yield curve, because the curve would be steeper in the absence of these policies. As such, we view the inversion of the 2y-10y yield curve (or other long-term spreads such as the 3m-10y) as little cause for alarm by itself.

Near-term spread is a better predictor of recessions than the 2y-10y

The Fed published a analysing the various yield curve measures and their predictive value of recessions. It found that the 18m forward implied T-Bill yield minus the current 3m T-Bill yield statistically outperformed longer term yield curve measures in predicting recessions, while having the advantage of not being subject to the same term premium issues that the longer-term yield curve has. This also has an intuitive logic – the 18m forward implied 3m yield gives an indication of whether the market thinks the Fed would be cutting rates in 1.5-2 years’ time if it is lower than near-term rates. This so-called near-term spread is now historically high, i.e. nowhere near inversion, and suggesting a low risk of recession. We would only add one important caveat in the current environment, which means we cannot draw too much comfort from this: inflation is far above the Fed’s target, and the market could take the view that even with a recession, the Fed would not be easing policy as its priority is to bring inflation back to target. Put another way: we do not as a base case expect a US recession (although ), but the fact that the near-term yield spread is sharply positive does not rule out a recession either.