Cooling US labour market supports Fed pause

Job vacancies have fallen significantly in the US, bolstering the case for both a softer landing for the economy, and a peak in interest rates.

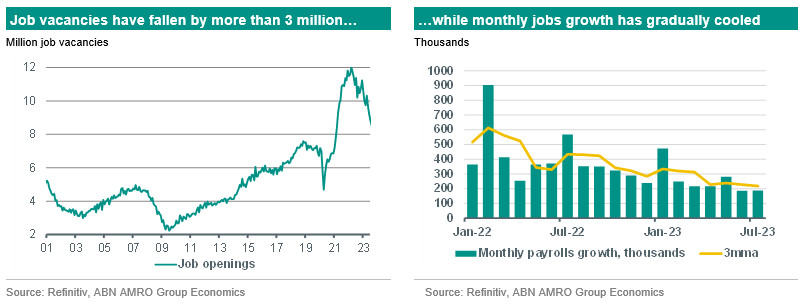

Labour market tightness continues to ease…

‘Soft landing’ expectations were bolstered yesterday by the JOLTS job vacancy data for July, which showed a decline in vacancies of around 300k as well as a downward revision to the June data, also by around 300k. As shown by this report, the JOLTS data is highly prone to revision, and so we cannot put too much weight into a single report. However, the broad trend of the past year has been for a sharp fall in vacancies, from a peak of around 12 million vacancies in March 2022, to 8.9 million as of the July data. Remarkably, this fall has so far occurred without any rise in the unemployment rate, which remains at a historically low 3.5%. With that said, alongside falling vacancies we have seen a gradual decline in monthly jobs growth – from an average 313k monthly gain in Q1 23, to an average 218k monthly gain over the past three months. We expect that decline to have continued in August when we get the latest payrolls data on Friday – we expect around a 150k gain in payrolls, which depending on participation could be enough to nudge the unemployment rate one tenth higher, to 3.6%. Over time, we expect this slowdown in jobs growth to intensify and to push the unemployment rate above 4% as we move into 2024.

…bolstering the case for no further Fed hikes

The JOLTS data supports our view that July was the final rate rise by the Fed of this tightening cycle. Fed Chair Powell has continually cited the job vacancy to unemployed ratio as a key metric of labour market tightness, which in turn drives the longer run inflation outlook. This ratio has fallen from a peak of 2.0 last year to 1.5 as of July – retracing more than half of the rise since the pandemic (in 2019, the ratio averaged 1.2). At the Jackson Hole Symposium last week, Chair Powell reiterated the Fed’s openness to raising rates if the recent rebound in some macro indicators persisted and inflationary pressure started to build again. In other words, Fed policy is now highly data dependent. In the near-term, alongside a continued cooling in the labour market, we also expect August core inflation data (released on 13 September) to be relatively benign. Taken together, this should convince the Committee to keep policy on hold when it next meets on 20-21 September. Beyond then, even with inflation expected to rebound temporarily in the Autumn, we expect a broadly slowing economy to keep rates steady for the next half year. We continue to expect the Fed to start cutting rates from next March, in order to offset the continued rise in real rates due to falling inflation. See our for more.