China - Tweaking our growth forecasts

Q1 GDP data (including upward revisions to past quarters) raise likelihood of reaching 5% growth target. We raise our 2024 growth forecast to 5.1% (from 4.7%), and cut our 2025 forecast to 4.5% (from 4.6%). Recovery still unbalanced and supply-side led; March activity data confirm property headwinds remain.

Sequential GDP growth accelerated in Q1-24, in line with our base case, benefiting from stimulus and a bottoming out in global manufacturing. However, the latest data confirm that the recovery is still unbalanced, with the supply side stronger than the demand side, and property still adding to headwinds. Meanwhile, risks from trade spats are rising.

Modest, technical changes in our growth forecasts for 2024/2025

In line with our base case, China’s real GDP growth accelerated in quarterly terms in Q1-24, picking up to 1.6% qoq (Q4-23: revised up to 1.2%). The upward revisions in the two preceding quarters resulted in annual growth coming in stronger than expected, at 5.3% yoy (Q4-23: 5.2%). We had already flagged in earlier publications that the balance of risks regarding our China growth forecasts has been improving for a while. Although domestic demand remains weak, and many challenges remain, Q1 GDP data raise the likelihood that the 2024 growth target of 5% will be within reach, also assuming further piecemeal monetary easing and targeted (fiscal) support. All in all, we raise our 2024 growth forecast to 5.1% (from 4.7%); this is more of a backward revision rather than a ‘game changer’ in terms of the outlook. Partly reflecting a stronger base from 2024, we cut our 2025 growth forecast modestly to 4.5% (from 4.6%).

Conflicting signals from March survey and hard activity data

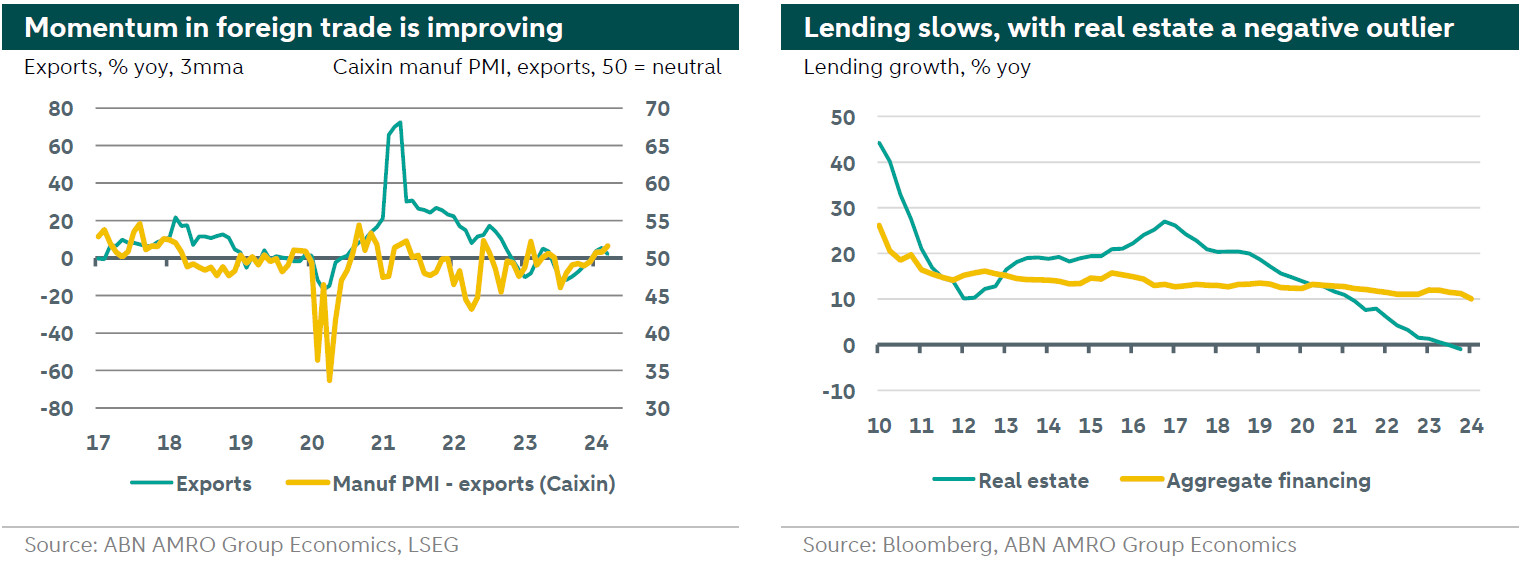

The latest macro data are a mixed bag. The rise of the official manufacturing PMI (NBS) in March did close the gap with Caixin’s equivalent, with both indices now back above the neutral 50 mark (see here). Services PMIs also picked up further, and the composite PMIs from both NBS and Caixin rose to ten-month highs. By contrast, the activity data for March generally signalled a softening growth momentum, with retail sales in particular on the weak side (see here). Property sector data remained lacklustre, suggesting that measures to stabilise the sector have not yet broken the negative feedback loop. Annual growth in exports and imports turned negative, but that largely reflected a base effect from the reopening last year, with underlying momentum improving on the back of a bottoming out in global manufacturing. Notably, the export components of both manufacturing PMIs have risen back to above 50 for the first time since February 2023. That said, risks from trade spats with the West are rising (see also this month’s Global View).

Annual lending growth dropped below 10% in March – for the first time in 25 years – as credit demand remains weak (real estate lending was a negative outlier). On the inflation front, CPI inflation fell back to a meagre 0.1% yoy – with upward pressure from the Lunar New Year period in February fading – while producer price inflation was negative for the 18th consecutive month. All of this reflects the fact that consumption and private investment still lag the overall recovery. We expect more piecemeal easing and targeted (fiscal) measures to support domestic demand going forward. Meanwhile, the fact that growth is structurally coming down and risks to central government finances are rising, led Fitch to put China’s sovereign rating on a negative outlook on 9 April, following a similar move by Moody’s in December 2023.