China - Recovery broadens, with property sector bottoming out

Growth target for 2023 of ‘around 5%’ in line with our expectations. China’s reopening rebound broadens, with retail sales firming and the property sector bottoming out. Support to remain targeted/piecemeal, as Beijing aims to contain leverage and prevent overheating.

At the National People’s Congress (NPC) early this month, the 2023 growth target was set at ‘around 5%’. This was in line with our expectation, but a bit below consensus (‘above 5%)’. Meanwhile, Beijing’s ‘around 5%’ target is close to our forecast of 5.2%. Another impression gained from the NPC is that policy support will be kept piecemeal and targeted rather than abundant/aggressive, as Beijing wants to keep overall leverage in check and avoid the overheating issues that arose after China’s rapid rebound following the original Covid-19 shock in 2020. The main risks to the outlook include: the slowdown in external demand, with recent bank turmoil in the US and Europe underlining the fall-out from unprecedented sharp rate hikes, and rising US-China tensions on tech, Taiwan and China’s position versus Russia – see also this month’s Spotlight.

China’s reopening rebound broadens

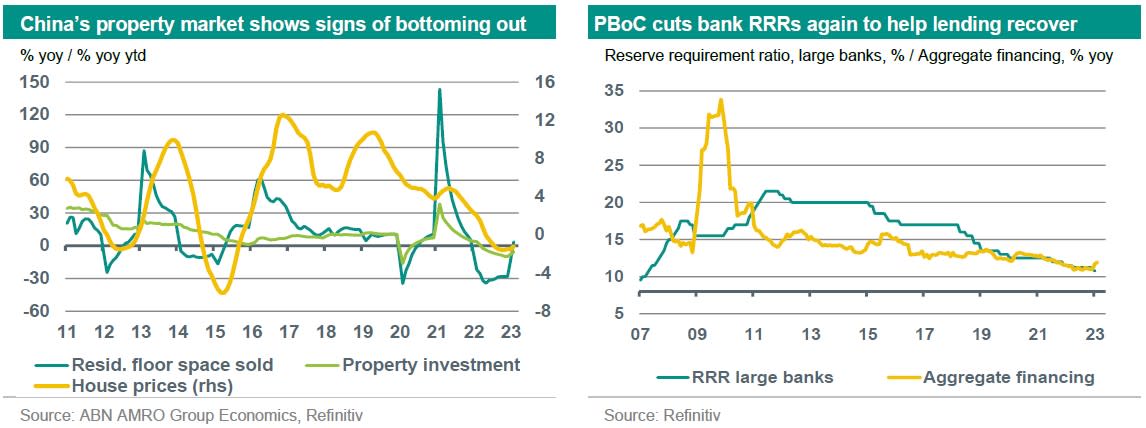

PMI and activity data published recently are in line with our view that China’s economic rebound resulting from the rapid Zero-Covid exit initiated in December 2022, is gaining strength and broadening. The rebound is led by the services sectors, which were hit the most by the combination of Omicron flare-ups and strict containment policy. This was illustrated by the February PMIs published early this month, with the services PMIs rising far above the neutral 50 mark. The latest activity data also showed improvement. Retail sales growth accelerated to +3.5% yoy in January/February (December: -1.8% yoy), confirming that private consumption, which was lagging during the pandemic, has the most catch-up potential. The fact that the property market, one of the key drags on the economy last year, is bottoming out, is also important in this respect. This is partly facilitated by more targeted support, coupled with the positive effects of the Zero-Covid exit. Residential property bounced back strongly in January/February, showing annual growth of 3.5% again for the first time since December 2021. Another sign of stabilisation is the turn in home prices, at least in the largest cities. Related to this is a cautious improvement in consumer confidence since the abandonment of Zero-Covid, though confidence remains at relatively weak levels for now.

Policy support to remain targeted and piecemeal, as Beijing still wants to contain leverage and prevent overheating

The policy proposals communicated at the NPC are in line with our view that Beijing will keep support ‘piecemeal’ and targeted rather than abundant/agressive. The formal budget deficit target was raised to 3.0% of GDP in 2023 (2022: 2.8%), with the broader consolidated deficit expected to be kept at around 7.5% of GDP. Infrastructure investment – typically used by Beijing as an instrument to ‘lean against the wind’ – will likely slow again, now that the economy is stabilising. On the monetary policy front, the inflation target was kept unchanged at 3%, with piecemeal easing and targeted support to safeguard liquidity and special lending programmes likely being maintained. The recent 25bp cut in bank reserve requirement ratios – in line with our expectations – also fits within this piecemeal easing approach. Specific policies to support consumption will also remain on the menu, as illustrated by recent measures taken at the local level to boost car sales.

This article is part of the Global Monthly of 27 March 2023