China - Balancing between pandemic control and supporting growth

Q1 GDP growth came in stronger than expected, but March/April activity was hit by lockdowns. We cut our near-term growth forecasts, but leave annual forecasts for 2022-23 unchanged for now. Containing Omicron the near-term priority; Beijing cautious and targeted with support; yuan corrects.

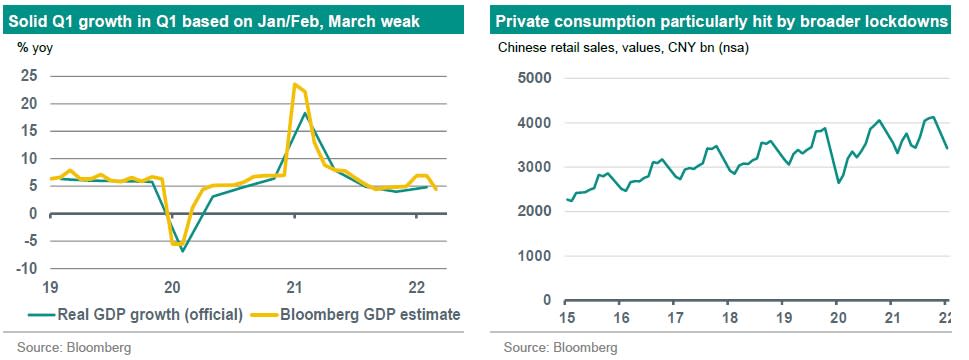

Q1 GDP growth surprised to the upside 4.8% yoy (consensus: 4.2%, ABN AMRO: 4.3%). Quarterly growth (1.3% qoq) slowed compared to Q4 21, but by less than expected. Growth was particularly strong in January and February. Widening lockdowns showed up in weak activity data for March, with more weakness expected for April. We had already incorporated pandemic drags into our forecasts, but have revised our near-term forecast lower again due to lockdowns. Still, we leave our annual growth forecasts for 2022 (5.0%) and 2023 (5.4%) unchanged for now. This assumes a stepping up of piecemeal, targeted support, but we continue to expect growth to be 0.5pp lower than Beijing’s formal growth target for 2022 (5.5%).

Impact of wider lockdowns hits March activity data; more weakness to come in April

In recent weeks, lockdowns in China have broadened as Omicron has spread. By 20 April, amongst the 100 largest cities, a group accounting for just over 40% of GDP was in full or partial lockdown. This has exacerbated headwinds and added to supply bottlenecks (see Global View for more). The impact of lockdowns is reflected in weak March data, with more weakness to come in April. All Chinese PMIs (from NBS and Caixin) fell below the neutral 50 mark, with both composite output indices dropping to the lowest levels since the initial covid-19 shock in February 2020 (although still not as much as they did back then). Industrial production, fixed investment and property investment slowed in March compared to Jan/Feb. Private consumption was hit particularly hard, with retail sales contracting by 3.5% yoy and by 1.9% mom sa. Lockdowns also brought an additional blow to the real estate sector, with residential sales dropping by 26% yoy in Q1. The weakening of domestic demand also translated into a slowdown in imports (-0.1% yoy), even though export growth remained strong (+14.7% yoy). Unemployment picked up to 5.8%, albeit remaining below the pandemic peak of 6.2% in February 2020. All this was also reflected in Bloomberg’s monthly GDP estimate, which slowed from 6.9% yoy in Jan/Feb to 4.4% yoy in March.

Balancing act between containing Omicron and economic stabilisation continues; yuan corrects sharply

The bar to fundamentally ease covid-19 policies in the near term remains high, with the leadership striking a balance between strict pandemic control and economic stability in a politically important year. This also means that reopenings will only be gradual. On the macro policy front, the PBoC recently announced a 25bp cut in bank RRRs, but refrained from rate cuts. This was in line with our view, as we anticipate the PBoC to wait until the covid-19 situation is more or less under control. What is more, the PBoC remains hesitant to ease monetary policy more broadly, with other major central banks on a hiking path. This is reflected in capital outflows and weakness in China’s stock markets and the yuan. Meanwhile, we expect Beijing to tolerate a further modest pick-up in credit growth, with targeted (fiscal) measures to offset the impact of lockdowns. On 18 April, the PBoC presented a support package with measures aimed at for instance helping local governments to step up infrastructure spending, compensating sectors most hit by the pandemic, and stabilising the property sector.