China - A tale of Trump risks, tariffs, and trade diversion

New trade tariffs under a potential Trump 2.0 are a risk to exports, currently a key engine of growth. Still, trade diversion (through countries like Vietnam/Mexico) mitigates effects of trade tariffs over time. Meanwhile, domestic demand remains weak; we cut our 2024 growth forecast to 4.9% (from 5.1%).

We cut our 2024 growth forecast to 4.9% (from 5.1%)

As expected, quarterly GDP growth in Q2-24 slowed from an above trend pace of 1.5% qoq s.a. in Q1 to 0.7% (see our earlier comments here), while annual growth slowed more than expected on revisions, to 4.7% yoy (Q1: 5.3%). We still expect some payback in Q3, but cut our 2024 annual growth forecast to 4.9%, from 5.1% (leaving our 2025 forecast at 4.5%). Meanwhile, the July monthly data point to a subdued growth momentum, with demand still hit by the property downturn. Retail sales picked up to 2.7% yoy in July (June: 2.0%) and 0.35% mom, but are still clearly lagging the pre-pandemic trend and industrial production (July: 5.1% yoy). Fixed investment slowed to 3.6% yoy ytd (Jan-June: 3.9%), with private investment at only 0.1% - driven down by an ongoing contraction in property investment. The surveyed jobless rate in urban areas rose to 5.2% (June: 5.0%), partly impacted by graduates entering the labour market.

External risks would rise under Trump 2.0, but trade diversion mitigates tariff impact

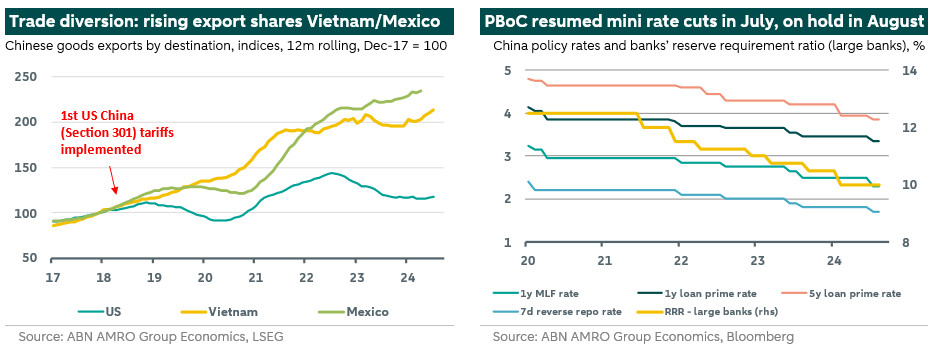

Exports are currently a key driver of growth, although export growth slowed in July. What is more, China’s supply-focussed strategy contributes to a broadening of trade spats, with the US/EU (and others) protecting strategic sectors against Chinese (over)supply. This risk would rise under a potential ‘Trump 2.0”. Trump threatens with a 10% universal tariff (see Global View) and higher (±60%), broader China-tariffs compared to his first tariff war in 2018-20. It is uncertain to what extent Trump will stick to these ‘promises’. Still, another tariff war would bring a faster US-China decoupling, although trade diversion (through countries like Vietnam or Mexico) mitigates the tariff impact over time (see chart). Meanwhile, although EU-China skirmishes continue (with China filing a WTO complaint against EV tariffs, and coming with a probe on EU dairy products), we still do not anticipate a broad China-EU trade war (also see here).

Beijing continues with (piecemeal) support, but more is needed to support demand

So far, policy easing did not really ‘move the needle’, with Beijing focused more on the supply than the demand side. Policy rates were cut (further) marginally in July, but kept on hold in August. This ‘piecemeal’ easing takes place amidst weak loan demand, with lending growth coming down. The PBoC is tweaking its monetary policy toolkit to make it more market-oriented, and introduced a form of (inverse) ‘yield curve control’ to put a floor under bond yields. With demand weak, inflation low, and the Fed expected to start cutting from September, we expect further RRR cuts and mini rate cuts going forward. Meanwhile, key focus of the CCP’s Third Plenum held in July was Xi’s (supply side) strategy of high-tech development, and self-reliance. More hints on support came from the Politburo meeting in late July, but recent measures to support consumption again primarily take the form of improving the supply of consumer services, rather than stimulate consumer demand. So far, the rolling-out of fiscal stimulus has been hampered by constraints at local governments, with the central government taking a stronger role. Last week, the housing regulator pledged to push forward with the plan (introduced in May) to let local governments buy homes from developers and turn them into affordable housing; progress on this front could help break the negative feedback loop in real estate.