Carbon Markets Strategist - Developments and outlook for European carbon markets

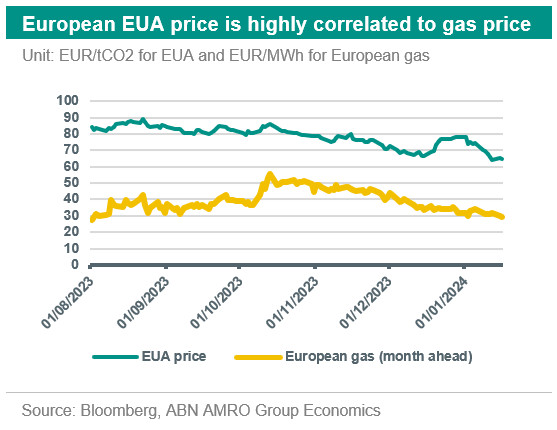

The EUA price has been witnessing a declining trend since the autumn of 2023, while it has also shown a high correlation with European gas prices more generally. The trends have continued this year, with the EUA price reaching a 15-month low in mid-January. Mild weather and slow economic activity reduced demand for ETS allowances from the power and industrial sectors. We expect the downward trend in EUA prices to continue in the near term on the weakness in the economy. January 2024 marks the extension of the European Emission Trading System to cover emissions from the shipping sector.

The EUA price has been experiencing a declining trend since the autumn of 2023, reaching a twelve-month low of 63.89 EUR/tCO2 mid-January. The decline was driven by a number of factors. First of all, the decrease in European gas prices. Lower gas prices trigger a switch from coal to gas for power generation, and since gas has a relatively lower emission intensity, demand for EUAs is lower for the same power generated. The correlation between gas and EUA price has been strong as seen in the chart below.

The mild weather the continent witnessed in the first half of this winter and the increase in the renewable share for power generation also played a role in reducing energy demand for heating purposes and reducing the need for conventional fossil based power generation. This in turn reduced the allowances needed for these uses.

Another factor affecting demand and putting downward pressure on the EUA price is the slowdown of economic activity. This is mainly driven by high interest rates which have been dampening aggregate demand and industrial output, and as a result, demand for allowances for power and industrial activities has been low.

From the supply side, primary markets have been on pause, with the last auction in 2023 took place on the 18th of December. Auctions started functioning again on the 15th of January 2024. Trading in secondary markets were suspended briefly due to public holidays. Accordingly, the EUA price trended briefly upward towards the end of 2023 driven by a combination of the annual pause in primary market and covering short positions by investment funds.

As of the 1st of January 2024, the extension of EU-ETS to the shipping sector enters into force. This means that every shipping company will have the responsibility to surrender allowances against the emissions of its fleet. The existing Monitoring, Reporting and Verification (MRV) system will be used to report and verify maritime shipping emissions. However, compliance and emission coverage will be gradually phased in, with 40% of emissions covered initially, 70% by 2025, and 100% as of 2026. Shipping companies will have to surrender allowances on the emissions they have reported in the previous year. Thus, starting from 2025, shipping companies have to surrender allowances for the first time for 2024 emissions. Moreover, there will be no free allocation of allowances for the shipping sector. Accordingly, an additional 80 to 100 million emission allowances will be added to the market. For more on this topic see our note .

Outlook

We expect the aforementioned trends to extend towards the first quarter of 2024, as the European gas market is witnessing an increase in confidence in bypassing this winter without any supply disruptions. This relief in gas markets is driven by mild weather forecasts and ample above seasonal storage levels (85%). Furthermore, as cuts in interest rates are only anticipated to take place from June of this year, we anticipate expectations of an improved economic outlook to start to build only later. Certainly indicators of the industrial sector suggest that weakness will persist in the near term, and as a consequence, we expect the weakness in industrial output to keep a downward pressure on EUA prices.

One upward factor on EUA prices is the upcoming surrender (of allowances) date by end of March. However, as the economic activity was slowed down in 2023, we do not think this impact to be quantitatively large. Rather, we expect it to be dominated by other forces. Also, secondary markets could witness some supply coming from companies selling off excessive allowances.

From the supply side, 2024 will witness an increase in allowances for different purposes. First, there will be additional allowances to cover the emissions from the shipping sector following its inclusion in the EU-ETS. Also, the front loading under REpowerEU package will continue in 2024, which will counter the impact of yearly supply cuts. These developments are expected to put the market in over-supply and limit any upward pressure on prices from the supply side.

Finally, we do not expect the upcoming inclusion of shipping industry to have an impact on EUA demand early 2024 as the surrender date will only take place in 2025. However, based on the positive economic outlook for the second half of 2024, as inflation flattens and interest rates start to be cut, we expect the allowances market to bottom up around May/June 2024.

Accordingly, our outlook for EUA is to average around 65 EUR/tCO2 in the first quarter of 2024. As we enter the second half of 2024, we expect EUA prices to start heading upwards reaching 80 EUR/tCO2 by year end.