Carbon Market Strategist - Will there be a supply correction?

Geopolitical escalations had their toll on EUA prices in April through their impact on energy prices. The supply surplus of allowances remains a factor that keeps a lid on EUA prices. The upcoming Total Number of Allowances in Circulation (TNAC) decision in mid-May is determinant to any shift in EUA prices thereafter. We do not expect any correction in EUA supply through the MSR mechanism as we think that the current surplus is temporary and will diminish in the long term.

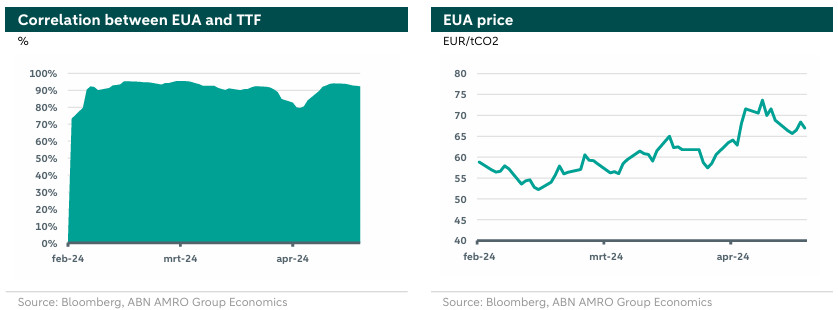

EUA prices averaged 65.7 EUR/tCO2 in April. The market kept an upward trend and witnessed high volatility in April that was fueled mainly by geopolitical escalations in Ukraine and the Middle-East through their impact on energy markets. EUAs are trading at 65.5 EUR/tCO2, at the time of writing. The oversupply in the market remains a factor that keeps a lid on EUA prices.

The EUA price has been highly correlated to European gas prices (see left hand chart below). Such correlation weighted heavily on the volatility of EUA prices in April. In its turn, European gas market has been responsive to geopolitical risks due to the tightness in the LNG global market. More precisely, the Russian attacks on Ukrainian gas storage facilities increased doubts on Europe’s gas storage for the next Winter. Also, the latest military escalation in the Middle-East between Iran and Israel and possible repercussions on LNG shipments from the gulf countries put gas traders on alert. Furthermore, attacks on ships in the Red Sea and unplanned maintenance in Norway have also participated in fluctuating the gas price. Consequently, volatility in EUA followed closely that of gas.

Meanwhile, published data on 2023 emissions in the European Union showed a reduction of 24% of emissions from the power sector compared to 2022 levels, thanks to mild weather and higher share of renewables in the power mix. Similarly, industry witnessed a decrease in its emissions of 7%, due to efficiency improvements and lower output following the slowdown in economic activity in 2023. The opposite happened in the aviation sector where emissions increased by 10%, which is attributable to the continuation of pandemic recovery in the sector. This data means that EUA demand to cover 2023 emissions around the surrender date coming September is going to be lower than budgeted.

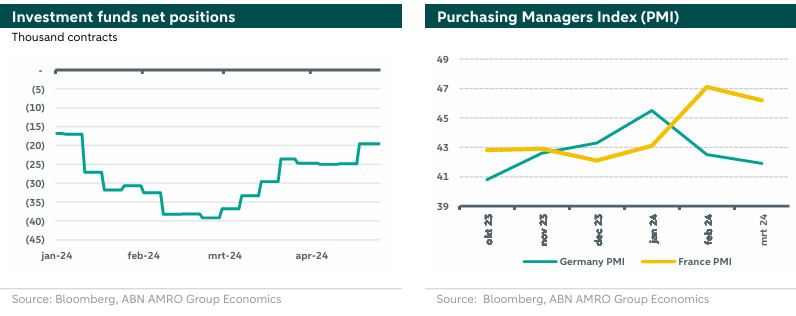

In 2024, from the demand side, the European manufacturing sector shows some signs of modest recovery, while the power sector is witnessing a lower output. Similar picture is reflected by the decrease in PMIs in the right hand chart below. Accordingly, the demand for EUAs for power and manufacturing purposes is still weak following the slowdown in overall economic activity and the rising share of renewables in the power sector.

In 2024, from the supply side, the ETS market is to witness a rise in auction volume by 76 Mt, compared to 2023, even though the overall cap is decreased by 100 Mt (down from 1486 Mt to 1386 Mt). The increase is mainly due to the front-loading of allowances to finance REPowerEU package, along with newly added allowances following the extension of EU-ETS to the shipping sector. Accordingly, the supply surplus in the market remains a factor that keeps a lid on EUA prices. However, one upcoming event regarding supply of allowances is the commission decision on the Total Number of Allowances in Circulation (TNAC) in mid-May, which will determine if there is any correction in the market supply through the Market Stability Reserve (MSR) or not.

Meanwhile, investment funds positions remain dominated by short trader as illustrated in left hand side chart above. However, the chart also manifests a decrease in bearish sentiments among investment funds since end of February.

Outlook

Considering market fundamentals, the bearish outlook dominates, with slow economic activity and industrial output, the end of the heating season, and the oversupply of allowances. However, the market remains vigilant and responsive to geopolitical developments through their impacts on energy markets, retaining a risk premium, along with the upcoming TNAC decision which could alter the market supply surplus.

We are skeptical that any changes in supply will take place by the MSR. We think that the current surplus is temporary and will diminish in the long term. Meanwhile, such surplus remains useful to mitigate the geopolitical volatility in the short term. Accordingly, our outlook for EUAs remains bearish with an EUA price to range between 60-65 EUR/tCO2 during May. If the commission decides to decrease the number of allowances in circulation, the price range will shift upward according the amount of EUAs withdrawn from the market.