BoE surprises with 50bp hike; more to come

The Bank of England surprised markets yesterday by raising its policy rate by 50bp. We expect further rate hikes given the re-acceleration in core inflation in the UK, but the pace and magnitude of further rate moves is highly uncertain and hinges on incoming data flow.

MPC hikes 50bp in response to shock inflation data

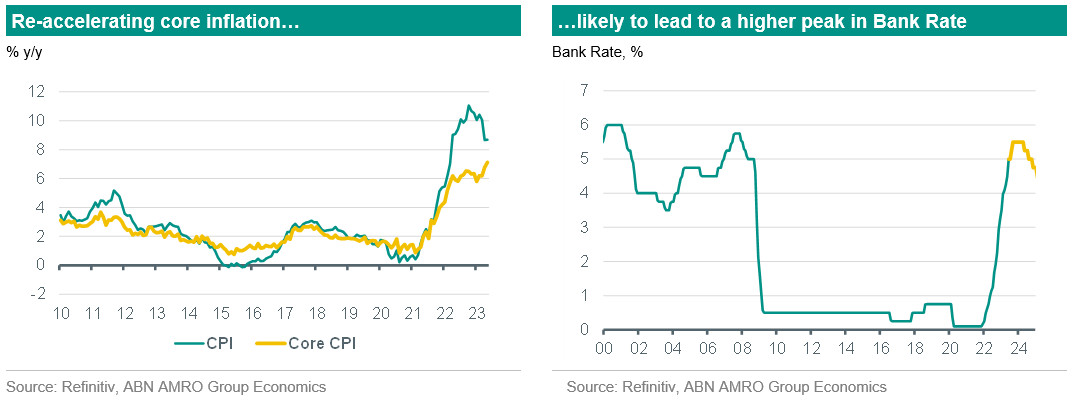

The Bank of England raised its policy rate by 50bp yesterday to 5.00%, a bigger rise than the 25bp we and consensus had expected. This followed a downshift to 25bp hikes at the past two MPC meetings. The move didn’t come entirely as a surprise given the upside surprise to the May core inflation data yesterday, which showed notable strength in labour-intensive services such as in restaurants and recreation categories – suggesting that the labour market is becoming a bigger inflation driver. The May upside surprise to inflation meant that the shock April reading was not as much of an outlier as it appeared, and combined with the upside surprises in wage growth – which is now running at 7.2% y/y – it points to the UK’s inflation problem getting worse rather than better (in contrast to recent trends in the neighbouring eurozone). Indeed, while headline inflation has trended lower on the back of falling energy prices, core inflation in the UK has re-accelerated after appearing to peak last September, and as of May had rebounded to 7.1% y/y, up from 5.8% in January. The Committee noted that services inflation is running some 0.5pp higher than it expected in its latest May projection, while the Bank’s latest Market Participants Survey showed inflation expectations increasing at the one- and three-year horizons (to 3.1% and 2.2%, from 2.7% and 2.0% previously).

We expect another 50-75bp in hikes, depending on the data flow

Following today’s hike and given recent data trends, we now see the MPC hiking further in the coming months, though the extent and magnitude of the tightening is highly uncertain and will depend on the incoming data. The MPC strongly hinted in its policy statement today that the 50bp move today was a one-off, as it refrained from reverting to the guidance of late last year that it would ‘respond forcefully’ if the outlook suggested more persistent inflation pressures. At the same time, while acknowledging the recent strength in the wage and inflation data, the June meeting minutes stated:

“There had nevertheless been some countervailing signs of softening pay growth. The KPMG/REC survey measure of pay for new permanent hires, which had historically led AWE [average weekly earnings] pay growth by around a year, had declined in May, having been broadly stable at a lower level since October 2022. This indicator pointed to a risk of private sector regular pay growth easing by more than had been expected in the May Report over the rest of this year.”

Given this, and the lags with which monetary policy affects the economy, we think the MPC will probably be minded to revert to a 25bp hike at August meeting, and for this to be followed by another 25bp hike in September (for now, we keep our expectation for modest rate cuts in H2 2024). This would mean a new peak in Bank Rate of 5.5% – well above our previous expected peak of 4.5%, but below current market pricing of a 6% peak. Still, we think the August decision will be a close call between a 25bp and a 50bp hike. The MPC is in full data-dependent mode, making near-term policy more liable to fluctuations as data comes in. If core inflation continues to surprise on the scale of the April and May readings, we think the MPC would have little choice but to hike by another 50bp in August, raising the prospect of a yet higher peak in Bank Rate.