Fed Watch – Easing cycle has ended

Following the hotter than expected inflation reading for January, we expect the Fed’s policy rate to stay on hold indefinitely, leaving the policy rate in restrictive territory. Lack of disinflation progress means the Fed will not be able to ease further before inflation gets a new impulse from tariffs. The labour market is unlikely to weaken so dramatically as to tip the dual mandate balance to easing.

Following the upside surprise in January CPI inflation, we no longer think inflation can come down sufficiently to allow the Fed to ease before tariff policy starts to push up inflation in the second half of the year. The most likely response to the combination of still elevated inflation - with significant upside risk on the horizon - and a relatively resilient labour market, is to keep rates on hold indefinitely. In addition to the downward pressure these restrictive rates continue to exert on inflation, keeping rates steady also minimizes the risk of the Fed having to reverse any further easing in response to inflationary Trump policy, making it a less confrontational path from a political perspective.

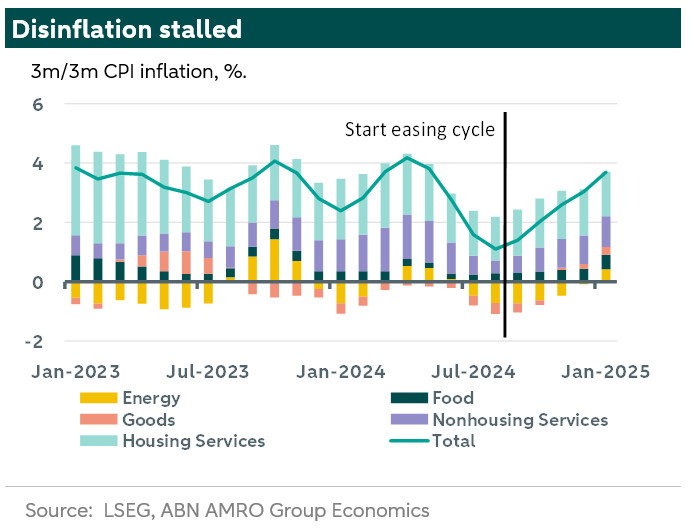

January CPI came in at 0.5% m/m for the headline and 0.4% m/m for the core measure. Due to more benign PPI data, our nowcast for core PCE of January is 0.3% m/m which would actually offer some progress on the y/y rate. The January inflation reading is known to be subject to considerable residual seasonality. January is a month where many companies increase their prices, but more so in some years then others. January surprises are therefore common, and indeed, we saw a similar picture at the start of 2024.

Generally, one should be careful in putting too much weight on a single reading. At the same time, the trend in inflation since the start of the easing cycle is clear. The Fed decreased rates by 50 bps when 3m/3m inflation was at a multi-year low, but it has since increased to levels nearing the upper end of the range over the past two years. Not reading too much into the January report therefore means that there is no reason to expect continued 0.4 or 0.5% m/m readings, but the broader recent trend makes it clear that we also should not be expecting readings consistent with a 2% y/y rate in the coming months. In the absence of tariffs, we would expect continued slow but steady progress towards target, as inflationary pressures from wages or housing have largely subsided. Third party data from Zillow suggests no renewed pressure on housing inflation, and the CPI has largely caught up to its level. Wage growth data, from for instance Indeed, remains moderate, and no significant source of inflationary pressure.

Over the course of the coming months, we expect to have clarity and first steps in the implementation of the various policies of the Trump administration. , we expect the tariffs to provide an inflationary impulse, continuing the need for restrictive rates. Changes in immigration policies, and abrupt shifts in federal hiring practices could significantly impact the labour market. Depending on their relative impact, the Fed may be pulled in either direction, or be forced to stay put. Our base case therefore sees the Fed on hold, with significant risks in both directions given the uncertain policy environment.