China: Some policy easing after a self-inflicted slowdown

Growth in Q3 slows as expected; some pick-up in quarterly growth foreseen in Q4. With rising headwinds from real estate and energy, we expect some policy easing to support growth. Commodities have driven PPI up, but record gap between PPI and CPI confirms limited passthrough.

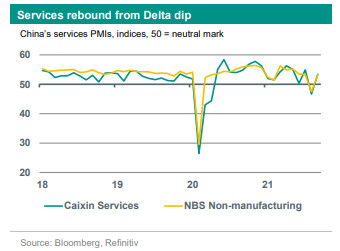

As expected, GDP growth slowed significantly in Q3, falling to 0.2% qoq sa (Q2: 1.2%) and 4.9% yoy (Q2: 7.9%). The key driver of the slowdown was the imposition of regional lockdowns and mobility restrictions following the Delta outbreak in July. This had a significant, though short-lived, impact on activity in the services sector. With restrictions being eased, the full-vaccination rate now at 75% and export strength continuing, we expect a pick-up in quarterly growth in Q4, also assuming further piecemeal policy support. Still, headwinds have risen in real estate (with the Evergrande crisis adding to this sector’s slowdown) and from a power crunch. These headwinds – also visible in a further slowdown of industrial production and investment – are to a large extent ‘self-inflicted’, following measures to reduce risks (real estate) and pollution (power). We leave our growth forecasts for 2021 (8.3%) and 2022 (5.5%) unchanged for now, but risks remain tilted to the downside.

Some easing of policies in the pipeline

While the growth target for 2021 of ‘above 6%’ will certainly be reached, policy inaction would raise the risk of annual growth in 2022 (our forecast: 5.5%) falling below Beijing’s preferred trajectory. The 2022 target will be announced at the annual National People’s Congress in early March 2022, although a glimpse of the government’s intentions may be spotted during the Central Economic Working Conference in December. We still expectanother 50bp RRR cut in the coming months (with the PBoC continuing to safeguard overall liquidity with special operations) and moderate fiscal support – by increasing the room for local governments to step up infrastructure spending. On the energy front, although the government has expressed its commitment to longer-term environmental ambitions, various measures have been taken to safeguard energy provision during the winter season. Coal production has been ramped up again, electricity prices have been liberalised somewhat, and power shortages have significantly reduced. Meanwhile, authorities have stepped in to stop the rise in coal prices.

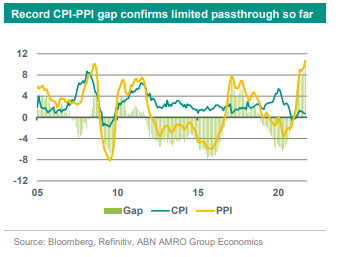

Producer price inflation at record high, but basically no pass-through yet into headline and core CPI inflation

Producer price (PPI) inflation rose further in September, to reach a record high of 10.7% yoy (August: 9.5%). The renewed rise in PPI inflation over the summer was driven by commodity-related sectors, with a sharp rise in coal and other energy prices coming against a backdrop of production stops targeting energy-intensive industries. Recent government measures should help to ease some of these pressures, although annual PPI inflation will likely stay elevated in the coming months. Meanwhile, headline CPI inflation fell to a five month low of 0.7% yoy in September, driven by food prices, leading the gap between PPI and CPI inflation to a historic high of 10 %-points. Core inflation also remained subdued, at 1.2% yoy. All of this implies that the passthrough of higher PPI-inflation into consumer prices is still very limited, although there are some mild signals of an increasing passthrough. This should leave some room for a moderate policy easing to support growth.