Bad news for inflation

Core CPI inflation picked up further in February, rising 0.5% m/m, up from 0.4% in January, and the highest reading since last September. This almost brought to a halt the decline in annual core inflation, which edged down just one tenth to 5.5% y/y from 5.6% in January. Headline inflation in contrast continued to move more substantially lower, to 6% from 6.4%, helped by the lagged pass-through of significant declines in utility gas prices, which fell 8% m/m.

Core inflation stays stubbornly firm…

The strength in core inflation was driven by shelter and core services, with recreation and car insurance making the biggest contributions to the latter. In contrast, core goods disinflation continued, while medical services continued to make a negative contribution due to a methodological quirk that is likely to continue weighing on inflation over the coming months.

…with more to come in the pipeline

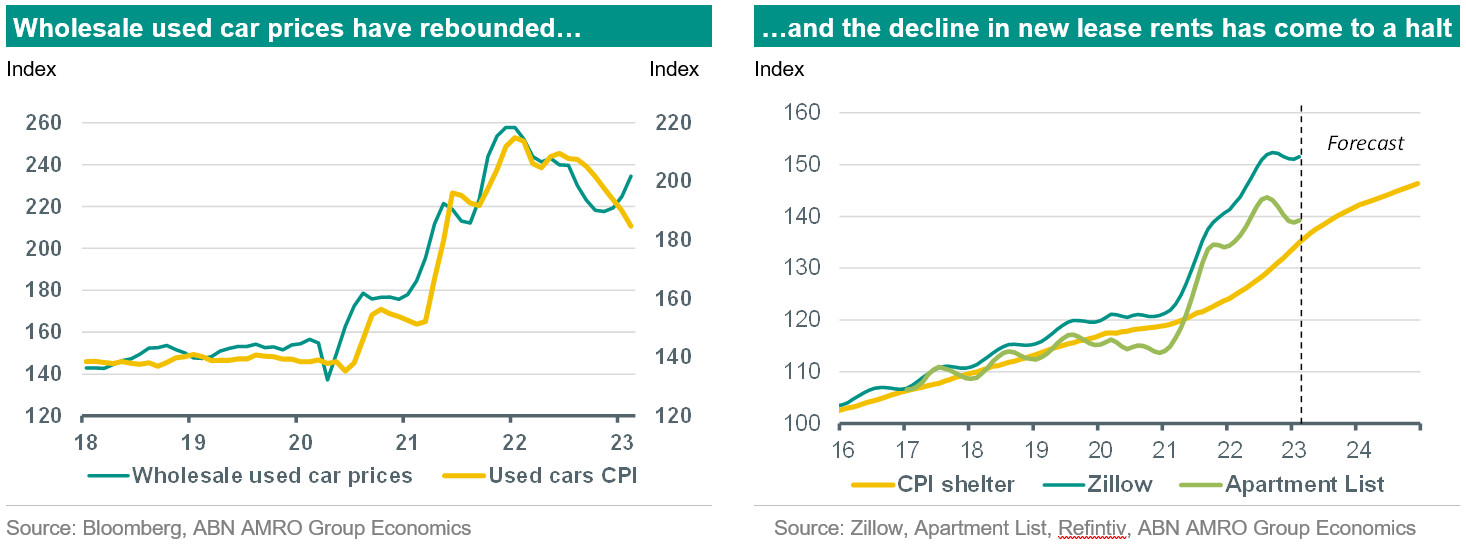

We expect m/m core inflation readings to remain stubbornly firm for at least the next 2-3 months. The core goods disinflation of the past few months is expected to go into reverse, given the rebound in wholesale used car prices. Core services inflation is also expected to remain firm, given persistent strength in unit labour costs. At the same time, the risks to the medium term inflation outlook unfortunately appear to be building again; incoming rental data for new leases suggests that the decline in housing rents may have come to a halt, with rents in February showing a modest rise following 4-5 months of consecutive m/m declines. Changes in rents pass through to the shelter component of the CPI with a significant lag. As such, shelter inflation was in any case expected to remain firm for the time being on the back of pass-through of last year’s rent rises. While it is early days, the latest data suggests that any reprieve in the shelter component might be short-lived.

Fed to hike 25bp next week, assuming market turmoil subsides

Following the publication of the February inflation report, market pricing for the 21-22 March FOMC meeting staged a recovery, with markets now pricing a 80% chance of a 25bp hike. Our base case is that the Fed indeed hikes by 25bp next week, taking the target range for the fed funds rate to 4.75-5.00%. This assumes that market conditions continue to ease over the coming days following aggressive moves by the authorities to stem the fallout from the SVB failure.